Looking for a set of church growth strategies that actually work? Ready to ignite a spark that sets your community ablaze with faith and fellowship? If your heart is shouting “yes,” you're in the right place!

Welcome to an epic journey where we unveil 35 powerful strategies, each a proven game-changer, ready to turbocharge your church growth. This comprehensive guide is your roadmap to a future brimming with potential, with strategies and guidance on how to grow your church.

Get ready to dive into the depths of market research strategies, learn how to convert visitors to new members, master church outreach strategies, church management solutions, inspire generosity through effective stewardship and discover the tools you need to accomplish unprecedented church growth.

Table of Contents

- The Motivation for Church Growth

- Church Growth Strategies

- Market Research Strategies

- Planning Strategies

- Church Marketing Strategies

- Strategies to Convert Visitors to Members

- Church Outreach Strategies

- Strategies to Build a Church Budget

- Church Technology Strategies

The Motivation for Church Growth

Before getting into how to grow your church, you want to be sure of the “why.” Church growth will look different for each congregation because each has distinct goals.

What Does the Bible Say About Growth?

There are at least nine Greek words in the New Testament to describe “growth.” The most commonly used one, "auxano", has several different meanings.

In scripture, it usually refers to the physical growth of plants or people. For example, “Consider the lilies of the field, how they grow” (Matthew 6:28).

However, the same Greek word is used to describe other instances of increasing or multiplying. For instance, Acts 6:7 says, “The word of God continued to spread.” A third usage of the term can be found in Ephesians 4:15, among other verses: “[w]e must grow in every way to become him who is the head, into Christ.”

Meaning of Church Growth

In general, you could say that the “Great Commission,” to spread the Gospel throughout the world (Matthew 28:18-20), is the goal of any church. There are innumerable ways to do that. How your church fulfills “going into the world and making disciples” depends on what your church and its members are called to do.

It helps to have a broad definition of “church growth.” Think of it as an open-ended church strategy, rather than a specific set of objectives. The point here is to ensure that church growth does not only mean getting bigger for the sake of getting bigger.

In fact, church growth may not mean more people at all. It could mean doing more or getting the right people to commit to important ministries.

For instance, you may have plenty of members, so adding more members to your congregation is not a priority. Perhaps the goals laid out by the church are being left unfulfilled, and you want that to change. Your church growth strategy should reflect your definition. Most importantly, church growth cannot be a concept implemented apart from or in contrast to your church’s central theology and mission.

If church growth means changing people’s lives so they can foster a closer walk with God, then you will succeed. The seeds you sow will be returned to you in the harvest (Galatians 6:8-10).

Look at Your Church Mission Statement

One way to frame your church’s calling and conversations about how to put it into action is to develop a church mission statement or review your existing one. It may seem symbolic, but if you are unable to put down on paper what your church is about, you and your leadership team should back up and consider doing this first.

Go to your deacon council, vestry or another leadership group. Decide on a church mission statement that encapsulates the objectives of your church. It may be vague, but it is vital to moving forward.

Once you have that statement, organize your strategies for church growth around it.

.png?width=488&height=167&name=MicrosoftTeams-image%20(4).png)

Church Growth Strategies

Now that you and your congregation are clear about your mission, you can take steps to achieve it through church growth. Most of the information in this guide is pragmatic, but not all will apply to your church. Because there is no single formula for how to grow your church, be sure to make the strategies you adopt your own.

Now that you and your congregation are clear about your mission, you can take steps to achieve it through church growth. Most of the information in this guide is pragmatic, but not all will apply to your church. Because there is no single formula for how to grow your church, be sure to make the strategies you adopt your own.

The best way to categorize church growth tools is by looking at people and programs. But before we do that, here are some basic things you can do to stimulate church growth without forming a committee or spending a dime.

Market Research Strategies

Market research is a powerful strategy that helps you to evaluate the viability of your church growth tactics. It offers a wealth of insight into your congregation, helping you understand their motivations and needs and how best to meet them. But how exactly can you harness the power of market research? Take a look at five tried-and-true church growth strategies for market research.

- Consider Your Target Demographics

- Conduct Surveys

- Be Aware of the Latest Data and Trends

- Look at What Other Churches in Your Area Are Doing

- Create Focus Groups

1. Consider Your Target Demographics

One general thing to think about when working to promote church growth is the demographics you want to reach in your community. They are unique to your church and where it is located.

Perhaps you have an older congregation and want to attract younger people to join. Maybe you have a diverse congregation age-wise but are lacking families with children.

Is there a military base nearby or is your church in a college town? The groups you want to appeal to dictate the strategies for church growth that you use to reach them.

Likewise, it can help streamline programs or identify those that may no longer be relevant to your church’s mission. If a ministry met its goals a long time ago, it may be time to direct those resources toward areas that are lacking them.

2. Conduct Surveys

Understanding what members and visitors want can help your church make key changes. Conduct church surveys to get answers to the questions your leadership team is asking. You don't need an expert researcher or a huge budget to get started. In fact, many programs allow you to create and manage surveys for free.

If you want to conduct a survey to better understand member and visitor needs and desires, check out this free guide, full of survey examples and instructions.

.png?width=488&height=232&name=MicrosoftTeams-image%20(5).png)

3. Be Aware of the Latest Data and Trends

Churchgoer attendance and giving habits have changed significantly over the last two decades. For your church to adapt to changes effectively, you'll need a strong understanding of the trends.

Our sleuths at Vanco spent hours on interviews and research to get the data you need on the latest trends in giving and attendance and key strategies to adapt to changes.

4. Look at What Other Churches in Your Area Are Doing

Ever wondered how some churches in your community seem to be flourishing, with pews full of enthusiastic worshippers every Sunday? What's their secret? How do they do it? The answer lies right around you — in your community and beyond!

Look Locally: The Power of Observation

The first step is simple: start observing. Visit the most vibrant churches in your community. What are they doing differently? What church growth strategies are they employing?

- Services: How are their services structured? What kind of music do they play? How do they engage their congregations?

- Programs: What programs do they offer? Are there specific ministries that attract people?

- Outreach: How do they reach out to the community? Do they have special events, charity drives or community service opportunities?

- Communication: How do they communicate with their members? Do they use social media, emails or a church app?

Remember, it's not about copying exactly what they do, but about understanding the principles behind their success.

Overcome Challenges: Implement New Tactics

Implementing new tactics might seem daunting, especially if you've never used them in your church before. But remember, every great achievement starts with a decision to try. Here are a few strategies for church growth to ease the transition:

- Start small: Instead of overhauling everything at once, begin with small changes. This could mean introducing a new song during worship or starting a new ministry.

- Engage your congregation: Get your congregation involved. Seek their input and make them part of the change.

- Stay consistent: Consistency is key. Stick with the new changes even if they don’t seem to work immediately. Growth takes time.

- Measure success: Keep track of what's working and what's not. Make adjustments as necessary.

Remember, the journey of a thousand miles begins with a single step. Start by observing and learning from other churches in your community. Then, take that first step toward implementing new church growth strategies. It might seem challenging at first, but with persistence and faith, you'll start seeing the fruits of your labor.

5. Create Focus Groups

Have you ever experienced the sheer power of collective wisdom? The kind that emerges when diverse minds come together, each contributing a unique perspective? If you haven't, it's time to introduce focus groups into your strategies for church growth.

Setting up a focus group isn't as complex as you might think. Here are some simple steps to guide you:

- Identify your objective: What do you hope to learn from your focus group? Are you looking for feedback on a new program? Ideas for community outreach? Clarity is key.

- Select participants: Look for a diverse cross-section of your congregation. Seek out different ages, backgrounds and perspectives to enrich the discussion.

- Choose a facilitator: This should be someone who can guide the conversation effectively, ensuring everyone's voices are heard.

- Prepare questions: Your questions should be open-ended, designed to spark discussion and delve deeper into the topic at hand.

- Set the date: Choose a date and time that works for most participants. Remember, your goal is maximum participation.

Once you've conducted your focus group, it's time to interpret the data. Here are some best practices to follow:

- Look for patterns: Are there recurring themes or comments? These could indicate areas of consensus or concern.

- Consider the context: Remember, comments are influenced by personal experiences and biases. Always keep this in mind when interpreting feedback.

- Don't ignore outliers: Sometimes, the most valuable feedback comes from the least expected places. Don't dismiss unconventional ideas too quickly.

And what about pitfalls? Here are some to avoid:

- Overgeneralization: Remember, a focus group is a small sample of your congregation. Be cautious about applying these insights to everyone.

- Ignoring negative feedback: It can be tempting to focus only on the positive, but negative feedback is equally valuable. It can highlight areas for improvement.

Planning Strategies

Ever found yourself gazing at a vibrant sunset, feeling invigorated, inspired, ready to conquer the world?

That's the power of dreams. But before your dreams for how to grow your church can take flight, you need a detailed plan. That’s why we’ve outlined a few church growth strategies to help you get the blueprint you need to succeed.

6. Create a Strategic Plan

Ever wished you had a roadmap to guide you? That's where strategic planning comes in. It's your compass, your guiding star, steering your church toward success with clarity and purpose.

Strategic planning isn't just important, it's essential. It keeps your church on track, ensuring you're moving toward your goals, not getting sidetracked. It helps you allocate resources effectively, manage change and measure success.

So how do you create this roadmap? Here are the steps:

- Assemble your team: Gather a group of dedicated, diverse individuals who can bring unique perspectives to the table.

- Assess your current situation: Conduct a SWOT analysis to identify your strengths, weaknesses, opportunities and threats.

- Visualize your desired outcome: Where do you want your church to be in five years? Ten years? Define these goals clearly.

- Craft your business plan: This should include your mission statement, market research and a church marketing plan.

- Create your vision statement: What's your church's ultimate goal? What's your purpose? Define it in your vision statement.

- Define your church's current role: How does your church serve its congregation and community right now?

- Outline your budget: Financial stability is key. Make sure your plans align with your financial capacity.

- Expand stewardship efforts: This involves resource management, financial stability, vision alignment and transparency.

- Set leadership criteria: Define what qualities you're looking for in your church leaders.

- Establish policies and procedures: These will guide your church's day-to-day operations and decision-making processes.

Remember, your strategic plan should be SMART — Specific, Measurable, Achievable, Relevant and Time-bound. This ensures your goals are clear, achievable and aligned with your vision. If you’re looking for more details on SMART goals or additional aspects of the planning process, visit our free guide on church strategic planning for more details.

7. Establish Your Brand

Now more than ever, branding is crucial for churches , especially because church membership has seen a significant decline over the past two decades.

Branding is more than just a logo or a catchy tagline. It's your church’s unique identity, its DNA. It's that ineffable quality that sets you apart and makes people choose your church over countless others.

So, how do you create this magical brand? Here's a step-by-step guide:

- Define your mission and vision: What's your church's purpose? What do you hope to achieve? Your brand should reflect these aspirations.

- Identify your core values: What principles guide your church? These values are the heart of your brand.

- Know your audience: Who are you trying to reach? Understanding your audience is key to crafting a brand that resonates with them.

- Create a unique visual identity: This includes your logo, color scheme, typography and imagery. These elements should be consistent across all your materials.

- Craft a compelling story: Every brand has a story. What's yours? This narrative should be woven into all your communications.

- Be consistent: Consistency is key in branding. Ensure a unified message across all platforms.

Remember, your brand isn't just what you say about yourself. It's what others say about you when you're not in the room. Make it count!

8. Be Realistic

As you set goals as part of your strategies for church growth, be sure they are reasonable. Consider the overall fiscal climate, especially where you live.

If the country is in an economic downturn or a big factory in your town just shut down, you should take these things into account. Think about the needs of the community and how the church can help meet them.

Take this into account when planning church growth strategies. For instance, when recruiting volunteers, recognize that people may already be stretched thin by other responsibilities. This is always a good thing to keep in mind, but especially during any tumultuous time.

9. Address Conflict Before It Emerges

Why is it so important to plan for and address conflict before it starts? Think about it. You're on an exciting journey — a journey of church growth. You're dreaming big, reaching out, making a difference. But what happens when conflict rears its ugly head? It slows you down, diverts your focus and saps your energy.

But imagine if you could anticipate these conflicts, prepare for them and address them head-on. Suddenly, they're not roadblocks anymore. They're stepping stones — opportunities for growth and learning.

So how do you plan for and address conflict before it starts? Here are some steps to guide your way:

- Understand the nature of conflict: Conflict isn't inherently bad. It's a natural part of human interaction. Understanding this can help you approach it with a more positive mindset.

- Anticipate potential conflicts: Identify areas where conflict may arise. This could be anything from leadership roles to resource allocation.

- Establish clear communication channels: Open, honest communication is key to preventing and resolving conflicts.

- Create a conflict resolution plan: This should include clear procedures for addressing and resolving conflicts.

- Foster a culture of respect and understanding: Encourage your team to respect diverse opinions and perspectives. This can go a long way in preventing conflicts.

- Train your team: Equip your team with the skills and knowledge they need to handle conflict effectively.

Still looking for additional resources to fend off conflict before it starts in your journey of church growth? Check out these two essential resources for more tips.

Church Marketing Strategies

In the digital age, church growth strategies have evolved beyond traditional outreach methods. Today, there are a plethora of tools at our disposal that can help us connect with more people, spread our message further and grow our churches like never before. The best part? Many of these tools are free or budget-friendly!

Whether it's harnessing the power of social media, engaging your congregation with newsletters, reaching out to a larger audience with YouTube, leveraging free church growth tools or even accessing Google's generous ad grants, the possibilities for how to grow your church are endless.

Ready to explore these strategies for church growth? Want to discover how you can use them to make your church a beacon of energy, a hub of community activity and a symbol of collective goodwill? Then keep reading, because we have a treasure trove of information coming your way.

- Use Social Media

- Publish a Newsletter

- Leverage YouTube

- Take Advantage of Free Google Ads

- Create an Email Blast

- Identify Church Marketing Strategies to Fit Your Budget

10. Use Social Media

If you are not already using social media to galvanize church growth, you are missing out on free and effective avenues for connecting with people. Approximately seven out of 10 adults in the United States are on Facebook. And popular new platforms now pop up every few months.

Social media is a great way to dispense information. A church event showing up in someone’s feed can catch their eye more easily than an e-newsletter. It’s a great way to reach new members because social media is designed for people to share events and information.

You might also branch out to new platforms. For example, Instagram and TikTok are ideal for reaching younger audiences. Be sure you are using each platform to reach the intended audience, rather than simply sharing the same post on another account.

Cast a wide net but be sure the content you are posting is of high quality — more is not necessarily more. It’s better to manage one or two platforms effectively than to have lots of accounts that get neglected. To help you create a powerful social media strategy check out our blog on How to Create a Church Social Media Strategy.

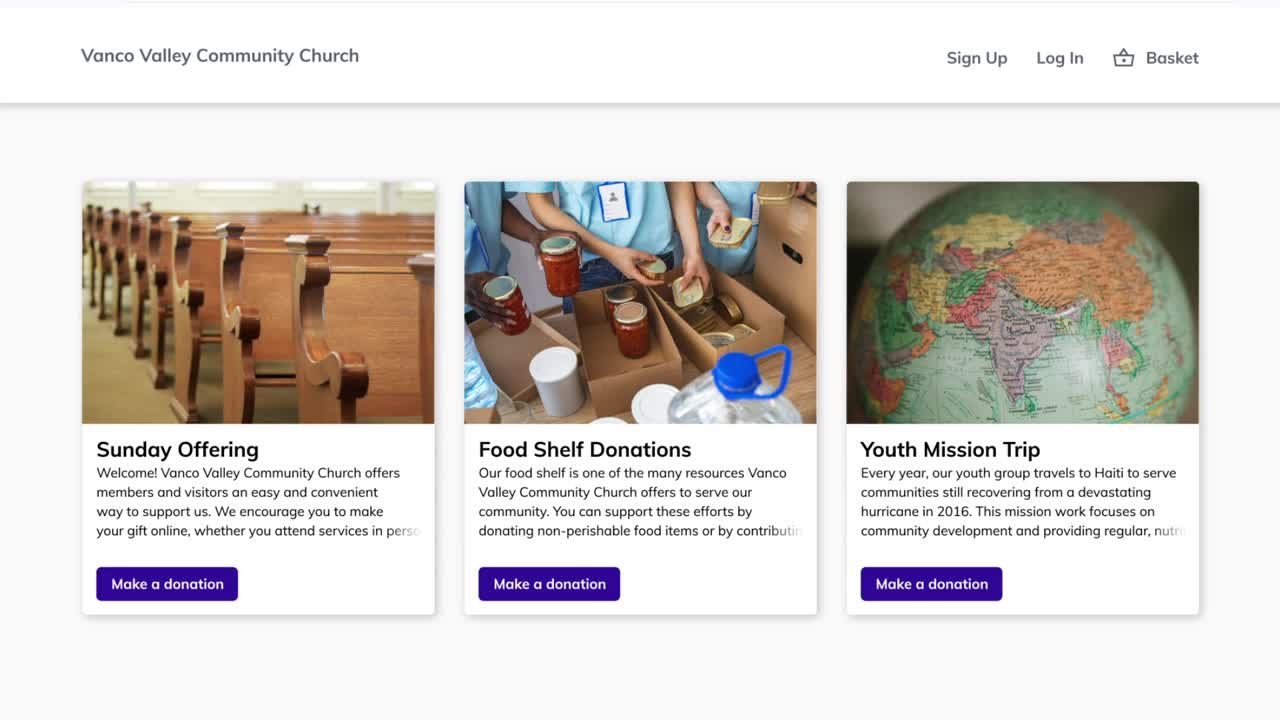

Also, be sure that your church’s website is updated and maintained. Search engines are still one of the most popular ways that people identify and get information about churches in their area. In fact, almost half of all Google searches are people trying to find local businesses. Seek the help of church members who know how to make the most of SEO for websites. Chances are someone in your congregation can help.

.png?width=576&height=246&name=MicrosoftTeams-image%20(6).png)

11. Publish a Newsletter

Newsletters are not just pieces of paper or digital notes. They are bridges connecting you with your congregation, new visitors and the community. They keep members informed, engaged and inspired. They're also channels of stewardship, encouraging members to contribute their time, talent and treasure for the greater good.

So how do you create an effective church newsletter? Here are ten best practices to guide you:

- Keep it concise: Less is more. Keep your content clear, concise and compelling.

- Discuss stewardship: Encourage members to contribute their time, talent and treasure.

- Make it easy to read: Use simple language, short paragraphs and bullet points.

- Engage your readers: Include testimonials, stories and interactive content.

- Include visuals: Photos can make your newsletter more engaging and personal.

- Digitize your newsletter: Reach out to a wider audience by using email marketing software and social media platforms.

- Don't forget about print: Some members still prefer printed newsletters. Don't leave them out!

- Support fundraising efforts: Use your newsletter to promote and support your church's fundraising efforts.

- Proofread: Ensure your newsletter is free of errors and includes all the necessary contact information.

- Name your newsletter creatively: A catchy name can make your newsletter more appealing.

Creating a newsletter might seem challenging, especially if you’ve never done it before. Luckily, there are plenty of tools that make it easy. If you need help getting started with this valuable church growth strategy, check out our free resource on church newsletters.

12. Leverage YouTube

One of the most overlooked church growth tools is YouTube. As the second largest search engine, churches can enjoy a lot of exposure for free. And because so many churches are already recording videos for their virtual worship services, it's easy to generate content for YouTube.

Marketing your church through YouTube is easier than you might expect. Use this free guide to get started.

13. Take Advantage of Free Google Ads

Imagine your church's name glowing brightly on the digital billboard of Google's search engine, a beacon guiding thousands to your community events. Can you see it? Now, what if you could do all this without stretching your budget? Sounds like a dream, right? But with Google's nonprofit ad program, it can be your reality!

Google's nonprofit ad program offers up to $10,000 per month in in-kind search advertising for eligible nonprofits.

That means your church's call for volunteers, funds and community engagement will reach a wider audience, sparking interest and inspiring action.

Whether you're partnering with local organizations or spearheading solo projects, this strategy for church growth can help your church be more than just a place of worship. It can be a hub of community activity, a beacon of energy and a symbol of collective goodwill.

How Do You Harness This Power?

So how do you qualify for this exciting opportunity? Here's the lowdown:

- Nonprofit status: Your church must be registered as a nonprofit organization holding valid charity status.

- Website requirements: You need a functioning website with substantial content that aligns with Google's eligibility requirements.

- Compliance with Google's rules: Your church cannot engage in certain prohibited activities outlined by Google.

From Qualification to Action

Once you qualify, how do you use Google Ads to amplify your church's impact? Here's your game plan:

- Define your goals: What do you want to achieve? More volunteers? Increased donations? Wider event attendance? Clear goals lead to potent church growth strategies.

- Target, target, target: Use keywords and demographics to ensure your ads reach the right people at the right time.

- Craft compelling ads: Make your ads irresistible. Be clear, be compelling and stay true to your church's mission and values.

- Monitor your progress: Keep an eye on your ads' performance. Adapt, tweak and improve for greater impact.

Running Google Ads can be daunting for beginners, but you don’t need to languish in frustration. We’ve built a free Google Ad Grant Guide for churches to help you get started.

14. Create an Email Blast

Email blasts can be a game-changer for your church. They can help you connect with visitors, inform them about your church's groups and events and encourage them to get involved. They can also inspire existing members to participate in outreach efforts, fostering a sense of community and shared purpose.

Ready to harness the power of email blasts as a strategy for church growth? Here are some best practices to guide you:

- Keep it simple: Don't overwhelm your recipients with too much information. Keep your message clear, concise and compelling.

- Personalize your emails: Use your recipient's name and tailor your content to their interests and needs.

- Use powerful subject lines: A compelling subject line can make all the difference. Make it intriguing, relevant and engaging.

- Include a clear call to action: What do you want your recipients to do? Join a group? Attend an event? Make it clear and easy for them to take action.

- Test and monitor your emails: Use analytics to track the performance of your emails and tweak your strategy for better results.

15. Identify Church Marketing Strategies to Fit Your Budget

Imagine your church reaching more people, impacting more lives and growing like never before. Can you see it? Can you feel the energy, the passion, the sense of shared purpose? Intrigued? Let's dive in!

Here are the top 20 church marketing strategies that can help you turn this vision into reality.

- Church website: Create a user-friendly, visually appealing and informative website. This is often the first point of contact for many potential visitors.

- Website SEO: Optimize your website for search engines to improve its visibility and reach.

- Local marketing for churches: Engage with your local community through events, partnerships and outreach programs.

- Google Ads for churches: Use Google Ads to reach a wider audience and attract more visitors.

- YouTube for churches: Share sermons, testimonials and other engaging content on YouTube.

- Social media for church marketing: Leverage platforms like Facebook, Instagram and Twitter to connect with your congregation and reach out to potential visitors.

- Church events and fundraisers: Organize events and fundraisers to engage your congregation and attract new members.

- Church advertising and marketing volunteers: Encourage volunteers to participate in advertising and marketing efforts.

- Worship livestreams and recorded services: Offer livestreams and recorded services to cater to those who can't attend in person.

- Church podcasts: Launch a podcast to share sermons, discussions and other inspirational content.

- Newsletters: Keep your congregation informed and engaged with regular newsletters.

- Welcome materials: Provide newcomers with welcome materials to make them feel valued and included.

- Church hospitality ministry: Foster a sense of community and belonging with a dedicated hospitality ministry.

- Paid church advertising: Invest in paid advertising to reach a wider audience and attract more visitors.

- Facebook ads: Use Facebook ads to connect with your target audience and drive engagement.

- Newspaper ads: Advertise in local newspapers to reach out to your local community.

- Signage: Use eye-catching signage to attract attention and draw in visitors.

- Direct mail advertising for churches: Use direct mail advertising to reach out to potential visitors in your local area.

- Christian marketing services agencies: Collaborate with professional marketing agencies that specialize in Christian marketing.

- Church blogs: Start a blog to share insights, updates and stories from your church. One way to create blogs quickly using existing materials is to convert your sermons into blog summaries. This video outlines how you can quickly build a blog in 10 minutes or less.

Looking for a deeper dive into the top 20 strategies? Check out our free church marketing guide for detailed how-to steps for each one.

Strategies to Convert Visitors to Members

One of the most important church growth strategies is to use the church building itself. Be sure your people and your facilities are ready to welcome visitors and potential new members with open arms and comprehensive church information and materials. These strategies for church growth can help.

- Offer Free Church Welcome Materials

- Create a Church Welcome Center

- Form a Church Welcome Committee

- Make Your Holiday Services Special

16. Offer Free Church Welcome Materials

Welcome materials are not just brochures or pamphlets — they are ambassadors for your church, a voice for your congregation and a reflection of your mission. What should these materials include? How can you make them effective, engaging and impactful? Here are the key elements every church should consider.

- Visitor information cards: These cards are a great way to gather information about your visitors and keep them informed about future events.

- Church information packets: These packets should include information cards, a schedule of church groups and events and where to watch past sermons online.

- Gifts: Small tokens like coffee mugs or candy can make newcomers feel welcome and appreciated.

- Thank-you notes: Personalized thank-you notes can make a lasting impression on visitors.

- Videos/photos of sermons: Provide visitors with a glimpse of your worship experience.

- Welcome letters from church staff: Warm welcome letters can make visitors feel valued and included.

- Upcoming events: Keeping visitors informed about upcoming events can encourage them to return.

- Stories from members: Sharing testimonials from members can showcase the impact of your church.

- Free food: Offering a free food item can add a personal touch to your welcome packet.

- Inspirational materials: Including inspirational quotes or verses can uplift and inspire visitors.

- Church ministries: Highlighting your ministries can help visitors find ways to get involved.

- Kids coloring book: Providing a coloring book can make families with children feel welcome.

17. Create a Church Welcome Center

Your church welcome center is the heart of your church and an important part of your church growth strategy. It’s the first point of contact for visitors and a crucial touchpoint in their journey toward becoming committed members. Why not make your welcome center the best it can be? Why not make it a beacon of hospitality and a hub of community spirit?

In addition to your church welcome materials, here are 11 proven ideas that can help you create a dynamic and memorable church welcome center.

- Clear purpose: Make it clear that the main purpose of your welcome center is to welcome and help newcomers.

- Easy accessibility: Ensure that your welcome center is easily accessible and is the first thing visitors see when they enter your facility.

- Inviting signage: Use attractive and inviting signs to make a great first impression on visitors.

- Warm hospitality: Offer meals and treats to visitors to make them feel welcome and at home.

- Friendly greeters and other volunteers: Train your volunteers to be warm, welcoming and helpful. They can set the tone for the entire visit.

- Interactive displays: Use interactive displays to engage visitors and provide them with information about your church.

- Comfortable seating: Provide comfortable seating to make visitors feel at ease and encourage them to stay longer.

- Children's corner: Create a dedicated area for children to make families feel welcome and catered to.

- Welcome videos: Use welcome videos to introduce visitors to your church and its mission.

- Church tours: Offer guided tours of your church to familiarize visitors with your facilities and services.

- Information desk: Set up an information desk where visitors can ask questions and get more information about your church.

Looking for more details on church welcome center ideas? Check out our free guide.

18. Form a Church Welcome Committee

Church welcome materials and a church welcome center are important resources for visitors and potential new members, but these programs need some guiding principles to make them work.

Your church welcome committee oversees the introductory process and plays a pivotal role in transforming first-time visitors into committed members. But how can you make this happen? How can you create an environment where everyone feels welcomed, valued and inspired? Here are seven proven ideas that can help you achieve this.

- Outstanding church website service: Create a user-friendly, visually appealing and informative website. This is often the first point of contact for many potential visitors.

- Easy parking: Ensure that your parking areas are well marked and easy to navigate. This can make a great first impression on visitors.

- Inviting atmosphere: Create an atmosphere that is warm, inviting and comfortable. This can make visitors feel at ease and encourage them to return.

- Exceptional childcare program: Offer a high-quality childcare program that is safe, engaging and fun. This can be a major draw for families with young children.

- Visitor-friendly sanctuary: Make your sanctuary a place where visitors feel welcomed and included. This can enhance their worship experience.

- Special greeting for visitors during the service: Acknowledge and greet visitors during the service. This can make them feel special and appreciated.

- Planned connections with visitors after the service: Encourage members of your congregation to connect with visitors after the service. This can foster a sense of community and belonging.

Looking for more tools to welcome guests as part of your church growth strategy? Check out our free church welcome committee guide.

19. Make Your Holiday Services Special

Christian holidays like Easter and Christmas are not just celebrations — they are golden opportunities to ignite church growth because new visitors often attend these services. But how can you leverage these holidays? How can you create services that stand out, draw crowds and boost engagement? Here are some ways to grow your church during holiday seasons.

- Creative sermon themes: Liven up your holiday services with sermon themes that resonate with the season's spirit. Think outside the box — how about a series on "The Gifts of Christmas" or "The Journey of Lent"?

- Interactive elements: Incorporate interactive elements like candle-lighting ceremonies, live nativity scenes, or Easter egg hunts to make your services more engaging.

- Inviting music: Use music to set the holiday mood. From traditional hymns to contemporary Christian songs, the right music can uplift, inspire and draw people in.

- Holiday-themed decorations: Deck out your church in festive decor to create a warm, inviting atmosphere that captivates visitors and members alike.

- Community outreach initiatives: Organize outreach initiatives like food drives, toy donations or caroling visits to local nursing homes to showcase your church's commitment to the community.

But don't just take our word for it. Let's look at some real-life examples. Church A transformed their Easter service into a community-wide event, complete with a sunrise service and breakfast. The result? Record-breaking attendance and a surge in new members. On the other hand, Church B's attempt to modernize their Christmas service with a rock concert-style worship fell flat, reminding us that understanding your congregation's preferences is key.

So you've attracted visitors to your holiday services. Great! But how do you keep them coming back? How do you turn these visitors into active members? Here are some tips.

- Follow up: Reach out to visitors after the holiday service with personalized notes or emails, thanking them for their attendance and inviting them to return.

- Connect: Provide opportunities for visitors to connect with your church community, such as small group meetings or social events.

- Invite: Extend a warm invitation for visitors to participate in your regular services and church activities any time of year.

According to Tony Morgan, a leadership coach for executive pastors, 90% of visitors returned if they received an immediate follow-up from someone in the congregation and 60% of individuals returned when the follow-up occurred within a few days.

Church Outreach Strategies

Once you have established plans for how to grow your church and your building and volunteers are ready, it’s time to connect with potential new members on a personal level. Here are some ideas for connecting with people in tangible ways, in addition to virtual church growth strategies.

- Ask for Member Referrals

- Target Your Outreach

- Focus on Members You Haven’t Heard From

- Focus on Children and Youth

- Hold Non-religious Classes

- Create Small Groups

- Create Inter-church Activities

- Sponsor or Partner with a Local Organization

- Plant a Church

20. Ask Members for Referrals

One simple thing you can do to grow membership is to encourage your congregation to invite friends or acquaintances to join them for worship or other church events. This may sound like a no-brainer but could be something you have overlooked.

Be specific. Ask your congregation to set a goal of asking one person a week to join them at a church event. This can go a long way to reaching prospective members.

You may want to include people who have been members of the church for a long time as well as newcomers. Both groups will be able to offer a perspective on what drew them to the church in the first place.

21. Target Your Outreach

Regardless of whether you are reaching out to existing or prospective members, be sure that you are focusing on people who are receptive to the call.

If you have been in the ministry even a short while, you know that you have to meet people where they are, but that goes both ways. Trying to convince people to do something that they are resistant to doing is fruitless. Look for members suited for the particular outreach and church growth strategies that match their interests and fit their schedules.

You also might consider forming a “church growth” committee, tasked with formulating an outreach plan. Be sure to have a diverse group to get a variety of perspectives.

Include creative people as well as those with pragmatic mindsets, who know how to get things done. Include younger members for insights into reaching that demographic.

22. Focus on Members You Haven’t Heard From

It’s easy to let people slip through the cracks. A friendly phone call, text or personal email will help you reconnect. And it could be an uplifting gesture to someone who is struggling during this time.

This doesn’t have to take an accusatory tone. Reach out to them to see how they are doing. If possible, ask them to become involved in a new or ongoing ministry.

To make this church growth strategy successful, be patient and remember Proverbs 21:5: “The plans of the diligent lead surely to abundance, but everyone who is hasty comes only to want.” The point is to be a steady, uplifting presence for your members.

23. Focus on Children and Youth

Research shows that churchgoing habits formed in childhood often carry into adulthood. This means that by focusing on children and youth as a strategy for church growth, your church can ensure its vibrancy and vitality for decades to come.

But how do you attract young people to your church? How do you make your church a place where they feel welcomed, valued and inspired? Try some of these strategies that have proven successful for many churches.

- Create engaging programs: Develop programs that cater specifically to children and young adults. Remember, one size does not fit all! Your programs should be age-appropriate, engaging and fun.

- Prioritize safety: Make child safety a top priority. This protects the children and reassures parents and builds their trust.

- Promote a positive image: Ensure that everyone in your ministry feels called to be there and that volunteers' roles are clear and meaningful.

- Cultivate a sense of community: Encourage involvement and foster connections. Make your church a place where kids and youth feel like they belong.

- Be unpredictable: Keep things fresh and exciting. Surprise elements can make your programs more engaging and memorable.

- Influence positively: Be quick to encourage and slow to criticize. Catch children doing something right and celebrate their achievements.

24. Hold Non-religious Classes

Offering free, non-religious classes or workshops taught by your own members who are experts in their fields can be a game-changer when you’re wondering how to grow your church. But why? What benefits does it offer? How can it boost engagement levels and foster growth? Let's break it down.

- Builds community: Classes and workshops provide a platform for members to interact, bond and build relationships, fostering a sense of community.

- Draws newcomers: Offering classes in areas like yoga, cooking or accounting can attract people who might not have otherwise visited your church.

- Showcases talents: Classes give members an opportunity to showcase their skills and talents, adding value to the church's activities.

- Creates value: By offering practical, useful skills, your church becomes a valuable resource in the community, encouraging more people to engage.

- Fosters a culture of learning: It promotes a culture of continuous learning and personal development within your congregation.

Now that you understand the benefits, let's explore ways to implement these ideas. How can you identify members who are experts in desired fields? How can you convince them to offer classes? Here are some ideas.

- Survey your members: Conduct a survey to identify the hidden talents within your congregation. You'll be surprised at what you discover!

- Create a win-win proposition: Show your members how teaching a class can benefit them — from improving their own skills to gaining recognition and respect in the community.

- Provide support: Offer resources and support to make it easy for members to conduct these classes. Remember, simplicity is key!

Next, how can you market these classes to your community? Here are some suggestions.

- Leverage social media: Use Facebook, Instagram and other platforms to spread the word about your classes.

- Host a launch event: Organize an event to introduce the classes and the instructors to the community.

- Use testimonials: Share testimonials from class participants to demonstrate their value and effectiveness.

To measure the efficacy of these classes, consider collecting feedback from participants after each class. This can provide valuable insights into what's working and what needs improvement.

Finally, let's talk logistics. How many classes should you offer? When should you offer them? What safety protocols should you follow?

- Start small: Begin with a few classes and expand as you gauge the response.

- Flexible timings: Offer classes at different times to cater to various schedules.

- Safety first: Follow all safety protocols, especially if the classes involve physical activities like yoga or cooking.

25. Create Small Groups

Small groups are more than just a trend. They're a proven strategy for church growth that fosters deeper connections, facilitates personal and spiritual growth and ultimately strengthens your church community. But what makes them so effective?

- Deep connections: Small groups provide a safe, intimate setting for members to share their thoughts, struggles and victories, fostering deep, meaningful connections.

- Personal growth: Discussions, Bible studies and shared experiences help members grow personally and spiritually.

- Community strength: By fostering a sense of belonging, small groups strengthen the overall church community.

Now that you know why they’re so important, let's investigate how you can tap into the power of small groups as one of your church growth strategies.

- Select effective leaders: Choose leaders who are passionate, empathetic and committed to fostering a positive group dynamic.

- Set clear expectations: Clearly communicate the purpose, goals and guidelines of the group.

- Promote effectively: Use your church's communication channels to inform members about available groups and how to join.

26. Create Inter-church Activities

Picture this: Congregations across your city, once isolated islands, now connected in a vibrant network of fellowship and mutual support. Imagine churches not just as individual entities, but as parts of an interwoven community, working together to lift each other up and make a real impact. Can you see it? This is the power of inter-church activities.

Here are just a few reasons why this is such a compelling answer to the question of how to grow your church.

- Unity in diversity: Through inter-church activities, congregations can celebrate their shared faith while appreciating their unique expressions of worship.

- Expanded reach: By partnering with other churches, your congregation can reach more people, amplifying its impact in the community.

- Shared resources: Partnership allows churches to pool resources, making it easier to undertake large-scale initiatives.

So now that you know what cooperation among churches can do for your church, let’s look at how you can tap into the transformative power of inter-church activities.

- Identify potential partners: Look for churches that share your values and are open to collaboration.

- Start small: Begin with a joint event or shared initiative and build from there.

- Communicate effectively: Use software to streamline communication, coordinate activities and keep everyone in the loop.

27. Sponsor or Partner with a Local Organization

In today's rapidly changing world, churches are constantly seeking innovative ways to grow and connect with their communities. One church growth strategy that has gained momentum in recent years is collaborating with local secular organizations. This approach can offer numerous benefits for church growth, but it also presents its fair share of challenges. What are the advantages and hurdles of partnering with secular organizations? What are some actionable steps for churches looking to embark on this exciting journey?

The Benefits of Collaboration

- Expanded reach: Partnering with secular organizations allows your church to tap into new audiences that you may not have reached otherwise. By working together, you can extend your influence and connect with individuals who may hesitate to engage in a traditional church setting.

- Community engagement: Collaborations with secular organizations demonstrate your church's commitment to the well-being of the community. This involvement can foster goodwill and trust among local residents, making your church a more attractive place for newcomers.

- Resource sharing: Secular organizations often possess valuable resources and expertise that can benefit your church's programs and initiatives. Whether it's access to facilities, funding opportunities or specialized skills, these partnerships can be a tremendous asset.

- Holistic ministry: Many secular organizations focus on addressing social issues such as poverty, addiction and homelessness. Partnering with them allows your church to engage in meaningful, holistic ministry, addressing both the spiritual and practical needs of your community.

The Challenges of Collaboration

- Differing values: Secular organizations may have missions and values that differ from those of your church. This can lead to ethical and theological dilemmas, so careful consideration and alignment are essential.

- Navigating boundaries: Maintaining a healthy boundary between the secular and sacred can be challenging. Striking the right balance between involvement and maintaining your church's identity is crucial.

- Communication hurdles: Miscommunication or misunderstandings can arise when working with organizations that have different communication styles or expectations. Clear and ongoing dialogue is essential to mitigate these challenges.

- Managing expectations: Not all partnerships will lead to immediate growth or success. It's important to manage expectations and be patient when embarking on collaborative ventures.

Practical Steps for Successful Collaboration

- Identify shared goals: Start by identifying secular organizations that align with your church's mission and values. Seek out shared goals that can serve as a foundation for collaboration.

- Build relationships: Establish personal connections with key individuals in the secular organizations you want to partner with. Attend their events, volunteer and engage in meaningful conversations.

- Create a memorandum of understanding (MOU): Clearly outline the scope of your collaboration, including roles, responsibilities and expectations. An MOU helps prevent misunderstandings and ensures everyone is on the same page.

- Maintain regular communication: Maintain open and consistent communication with your secular partners. Regular meetings and updates will help address any issues promptly and keep the partnership thriving.

- Evaluate and adapt: Periodically assess the impact of your collaborations. Be willing to adapt and refine your approach based on the results and feedback from both your church members and secular partners.

Resources for Church/Organization Collaborations

- Community networking: Use online platforms and local community networks to identify potential partners in your area.

- Interfaith or ecumenical groups: Consider joining interfaith or ecumenical groups that can facilitate connections with secular organizations.

- Training and workshops: Attend workshops or training sessions on partnership development and community engagement to gain valuable insights and skills.

Collaborating with local secular organizations can be a powerful strategy for church growth, but it requires careful planning, open communication and a commitment to shared goals. By navigating the challenges and leveraging the benefits, your church can expand its reach, make a positive impact in the community and grow in meaningful ways. Remember, building bridges takes time and effort, but the results can be transformative for both your church and the community you serve.

28. Plant a Church

“Church planting” is more than just establishing a new congregation. What makes it so effective as a church growth strategy?

- Reaches new communities: By planting new churches, you can extend the reach of your ministry to untouched areas.

- Enhances evangelism: New churches often have a heightened focus on evangelism, leading to more converts.

- Diversifies the community: Church planting allows for a diversity of worship styles and approaches, attracting a broader range of people.

Looking to tap into the transformative power of church planting? Here are some tips on how to grow your church this way.

- Target the right locations: Identify areas that need a new church.

- Conduct research and assessments: Gather data about the community and its needs and potential challenges.

- Find the right pastoral team: Choose leaders who are passionate, empathetic and committed to the vision of the new church.

- Cultivate a strong leadership culture: Foster an environment of empowerment, accountability and continual growth.

- Use an established new church checklist: Don’t start from scratch. See the comprehensive steps other churches have taken to make their plants a success.

Strategies to Build a Church Budget

To make any of your church growth strategies a reality, you must have a good understanding of your church’s financial condition. You will need financial resources to fund many of your growth strategies and existing and new church members expect transparent, efficient and honest financial management from your church. Learn more about key aspects of church finances here.

- Build a Clean Church Budget

- Increase Tithes and Offerings

- Optimize Fundraising

- Explore Alternative Revenue Streams

29. Build a Clean Church Budget

A church budget is more than just a financial plan. It's a strategic tool that can guide your church toward its mission, promote transparency and foster trust within your congregation. But how exactly can you create a clean church budget?

- Develop a budget plan: Start by outlining your church's financial goals, anticipated income and expected expenses.

- Monitor regularly: Regularly review and adjust your budget to ensure it aligns with your church’s mission and current financial status.

- Overcome challenges: Common challenges include unexpected expenses and fluctuating income. To overcome these, maintain a contingency fund and diversify your income sources.

How does this help? Let's hear from Pastor John from Church XYZ: "Our clean budget has been a game-changer. It's not just about better financial management; it's about greater transparency, increased trust, and stronger engagement from our congregation."

So, how can your church tap into the power of a clean budget as part of your strategy for church growth? Here are some tips.

- Leverage technology: Use advanced budgeting software to streamline your budgeting process, especially for larger congregations.

- Promote transparency: Make your budget accessible and understandable to all members of your congregation.

- Seek feedback: Encourage your congregation to provide feedback on the budget for continuous improvement.

Part of your church budgeting process is to be aware of potential pitfalls. These can include lack of long-term planning, underestimating costs and failing to align the budget with the church's mission. Navigating these challenges requires careful planning, wise counsel and a steadfast commitment to your mission.

If you’re looking for help, our team put together a trove of church budgeting materials and information, including the details on the different types of church budgets, questions to ask before creating a budget, items you should include in a church budget and a free template you can use. Access our church budget template and guide now to get started.

30. Increase Tithes and Offerings

A church’s financial health is often directly linked to the generosity of its congregation. As such, finding effective ways to increase tithes and offerings is vital for every church's growth and sustainability. Let's dive into some relevant strategies for church growth that can help.

- Embrace the power of vision: People are more inclined to give when they understand the “why” behind it. Therefore, instead of focusing on expenses, make money about vision. Share the impact of their giving, be it supporting community outreach programs, maintaining church facilities or funding missions.

- Cultivate a culture of generosity: Generosity should not only be encouraged during the offering time, it should be a value deeply ingrained in your church culture. Regular teaching on stewardship, sharing testimonies of generous givers, offering short prayers for tithes and offerings, and leaders modeling generosity are all powerful ways to foster this culture.

- Communicate regularly: Regular communication about the importance and impact of tithing can encourage more consistent giving. Whether through sermons, newsletters or social media, keep your congregation informed about how their contributions are being used.

- Run short-term giving campaigns: Organizing time-bound giving campaigns for specific projects or causes can motivate people to give more. Ensure these campaigns align with your church’s vision and communicate clearly how the collected funds will be used.

- Encourage commitment: Inviting congregants to commit to regular tithing can lead to an increase in giving. This could be through pledge cards or digital commitments via your church app.

- Practice transparency: Transparency about your church's financial situation and how funds are used promotes trust. Regularly share financial updates and consider having open meetings where congregants can ask questions.

With these church growth strategies, increasing tithes and offerings in your church is not only achievable, it can also strengthen the engagement of your congregation. Remember to introduce changes gradually, communicate effectively and always tie them back to your church's mission. As Proverbs 11:25 says, "A generous person will prosper; whoever refreshes others will be refreshed."

Monitoring your progress is as important as implementing these strategies for church growth. Keep track of changes in giving patterns, feedback from congregants and the overall impact on your church's financial health. The journey toward increased giving is a marathon, not a sprint, but with persistence and faith, you will reach your goal.

31. Optimize Fundraising

Fundraising is a lifeline for churches, enabling them to support their ministries, outreach programs and day-to-day operations. Let's explore some fundraising opportunities and best practices that can help churches reach their financial goals while aligning with their values.

- Identify fundraising opportunities: Each method has its benefits and potential risks, such as over-reliance on a single income source or alienating congregants with excessive fundraising. It's crucial to select church growth strategies that reflect your church's culture and values. That’s why our team built a comprehensive list of 114 fundraising ideas for churches that you can use for inspiration.

- Craft a compelling fundraising campaign: A successful campaign requires careful planning. Here are some steps to consider:

-

- Set clear goals: Concrete, measurable goals give direction to your campaign and motivate donors.

- Craft an effective message: Your message should communicate the need, explain the impact of donations and align with your church's vision.

- Reach potential donors: Use various channels — letters, social media, emails and face-to-face meetings — to connect with your congregation and beyond.

- Manage donations responsibly: Transparency in how funds are used builds trust. Regularly share updates about the progress toward the goal and the impact of donations.

- Show appreciation: Always thank your donors. Acknowledging their contributions fosters a culture of gratitude and encourages future giving.

- Maintain fundraising strategies over time: To ensure the sustainability of your fundraising efforts, regular evaluations are necessary. Assess what's working, what's not working, and adjust your strategies accordingly. Keep your congregation involved in the process, celebrate milestones together and continue to express appreciation for their generosity.

32. Explore Alternative Revenue Streams

While tithes, offerings and fundraising endeavors form the bedrock of a church's financial resources, diversifying revenue streams can significantly enhance fiscal stability and promote church growth. Just as families today often rely on multiple income sources, churches too can benefit from this approach.

- Pledge drives: Annual pledge drives are an effective way to secure commitments from your congregation for the upcoming year. Held at the end of the calendar year, these drives not only help in budget planning but also encourage responsible giving. Members tend to fulfill their pledges throughout the year, creating a reliable source of income. Online giving platforms enhance reliability, making it convenient for members to fulfill their obligations.

Action Tip: Implement online giving platforms to facilitate easy and consistent contributions from your congregation.

- Themed tiving: Organize giving campaigns around holidays, special events or theological themes. Themed campaigns can attract more contributions by tapping into the emotional resonance of specific occasions. Whether it's an Easter offering or a campaign centered on charity and stewardship, themed giving adds a unique touch to your fundraising efforts.

Action Tip: Promote themed campaigns through your church's communication channels and create compelling narratives around each theme.

- Sponsorships: Engage your community by seeking sponsorships for church-related events or causes. Whether that means sponsoring missionary families, helping underprivileged youth attend camps or funding specific church projects, sponsorships provide financial support while establishing meaningful connections with donors.

Action Tip: Develop sponsorship packages outlining the benefits to sponsors and create compelling pitches for potential sponsors.

- Memorials: Encourage members to consider leaving a portion of their assets to the church in their wills. This long-term strategy for church growth ensures that the resources members accumulate during their lives will continue to support the church's mission. Offer guidance on estate planning in an appropriate context to foster discussions about legacy giving.

Action Tip: Initiate conversations about legacy giving with your congregation, emphasizing the importance of planning for long-term sustainability.

- Targeted ministry campaigns: When your church has a specific need aligned with its mission, consider launching a targeted campaign. Members are often motivated to contribute when they can see their donations directly support a meaningful cause. Use committees, newsletters and social media to promote these campaigns effectively.

Action Tip: Clearly communicate the goals and impact of targeted ministry campaigns, ensuring transparency and accountability.

- Capital campaigns: Distinguish between targeted giving and capital campaigns. Campaigns focus on securing resources to bolster the church's overall mission and future needs. Set specific goals for these campaigns and ensure they align with your church's long-term vision.

Action Tip: Establish a dedicated committee or task force to plan and execute capital campaigns.

- Events: Organize events, from festivals to themed gatherings, to generate revenue and foster community engagement. Consider ticketed dinners, cookoffs, concerts or recurring events like oyster roasts. Events are excellent church growth strategies because they have the potential to attract both your congregation and a broader audience from the community.

Action Tip: Leverage the talent within your church and collaborate with local artists or musicians to make events more appealing.

- Services: Use available church facilities to offer services such as childcare, counseling, or "parents night out" events. These services can provide a valuable community resource while generating additional income for your church.

Action Tip: Advertise these services within your congregation and the local community to attract participants.

- Products: Consider establishing a church bookstore or coffee shop to sell religious materials or refreshments. Engage your congregation's creative talents by encouraging them to donate baked goods or artwork for sale. These initiatives can boost revenue while encouraging members to spend time at the church.

Action Tip: Ensure strategic placement of the store or shop to attract foot traffic.

- Grants: Explore grant opportunities from private foundations and government entities as a strategy for church growth. To qualify, your church should be registered as a 501(c)(3) nonprofit organization. Build relationships with local foundations and use online tools to search for potential grants.

Action Tip: Seek assistance from individuals with grant proposal writing experience to maximize your chances of securing grants.

- Investment capital: Manage your church's savings wisely by ensuring they earn the best possible return. Consult with financial advisors to determine suitable investment options while adhering to tax laws governing nonprofit organizations.

Action Tip: Establish clear financial goals and designate different accounts for specific purposes to manage funds effectively.

- Renting: Rent out church facilities to other nonprofit organizations or groups whose activities align with the church's mission. Ensure that any income generated from rentals complies with tax-exempt regulations.

Action Tip: Consult with your church's accountant to navigate tax implications and explore the potential of renting out available spaces.

- In-kind donations: Leverage your congregation’s skills and expertise to provide services that would otherwise incur costs. From accounting support to maintenance tasks, volunteer efforts can significantly reduce operational expenses.

Action Tip: Organize volunteer groups within your congregation to take on various tasks, ensuring a fair rotation to prevent burnout.

Church Technology Strategies

Now more than ever, technology in churches is essential to meet the needs and preferences of their congregations, streamline church giving and event processing, and ease the administrative burden on church staff. Churches can also expand their reach with virtual services. Consider all the ways that technology can be a powerful church growth strategy.

33. Take Advantage of Giving Technology

In today's digital age, technology has become an integral part of our daily lives and churches are no exception. Implementing church giving technologies streamline donations, increase revenue and foster a culture of generosity. Let's dive into five key giving technologies that can make a significant difference in your church's financial health and growth.

- Church giving pages: A church giving page is a website or a part of your church's website dedicated to accepting online donations.

Benefits: They offer convenience and flexibility to members, allowing them to donate anytime, anywhere. Automated recurring donations ensure consistent giving, even when members can't attend services.

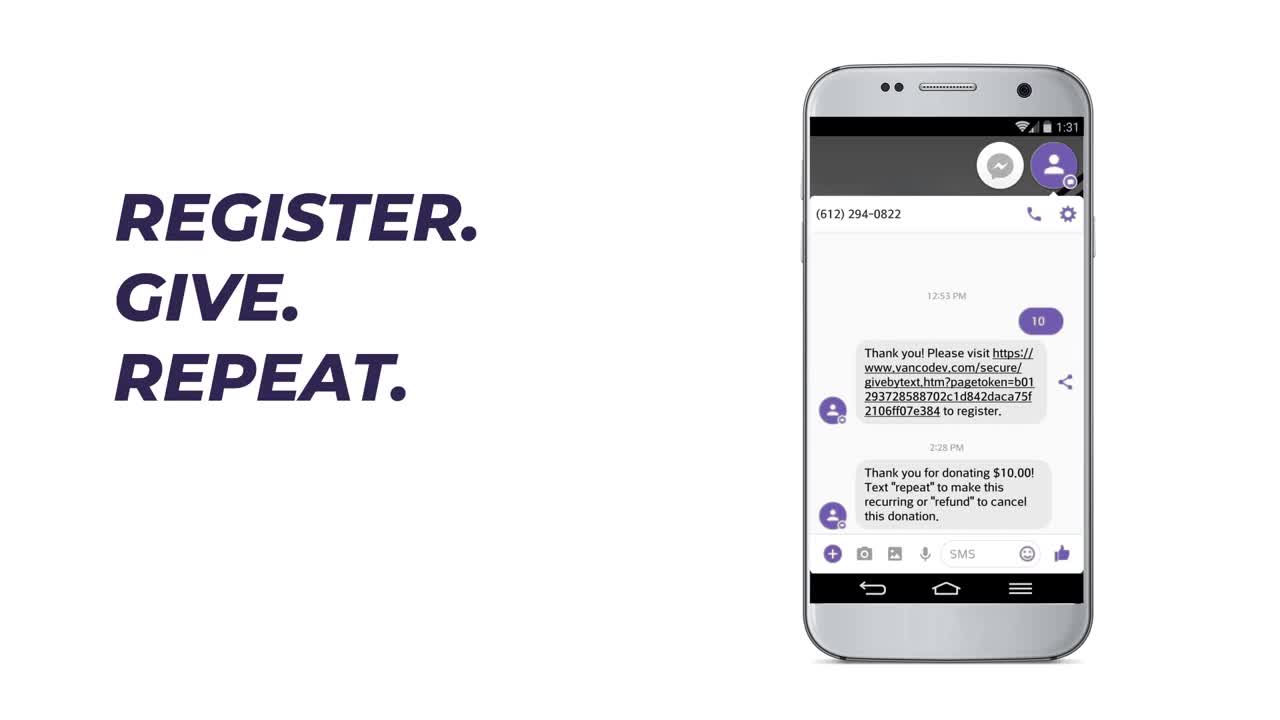

- Church text-to-give: Text-to-give allows congregants to donate using their mobile phones by texting a specific number or code.

Benefits: It's quick, user-friendly and perfect for impromptu giving during special events or appeals. Plus, it's accessible on any device that can send a text message.

- Portable card readers: Portable card readers enable churches to accept debit and credit card donations in person.

Benefits: They provide a convenient alternative for those who don't carry cash or checks, potentially boosting in-person giving.

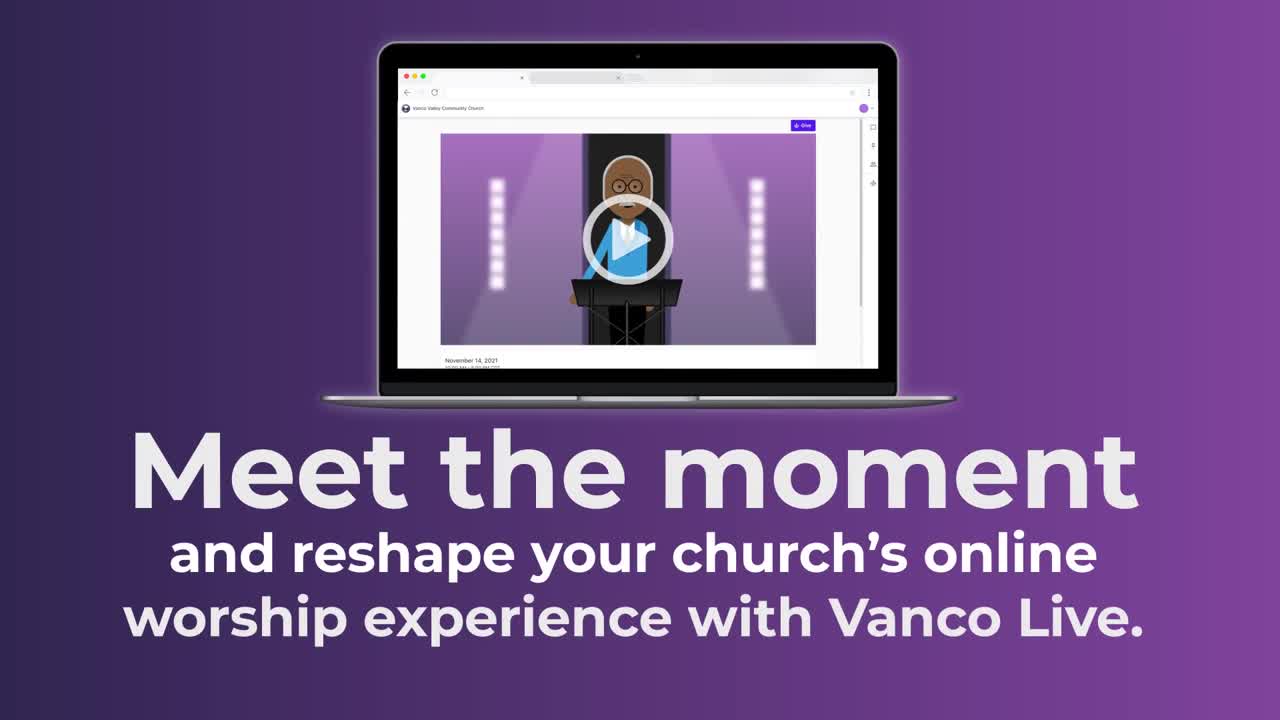

- In-livestream giving: In-livestream giving allows members to donate while watching livestreamed services.

Benefits: It's convenient and immediate, capturing the generosity of viewers in the moment. It also allows those watching from home to participate in the act of giving.

- Church event management software: Event management software can streamline ticketing transactions for church events.

Benefits: It simplifies the ticket selling process and makes it easier to manage event attendance. Some software options also provide features for promotion and communication.

-1.jpg?width=488&height=167&name=Vanco-Events-for-Free-CTA%20(1)-1.jpg)

34. Use a Fee Church Mobile App

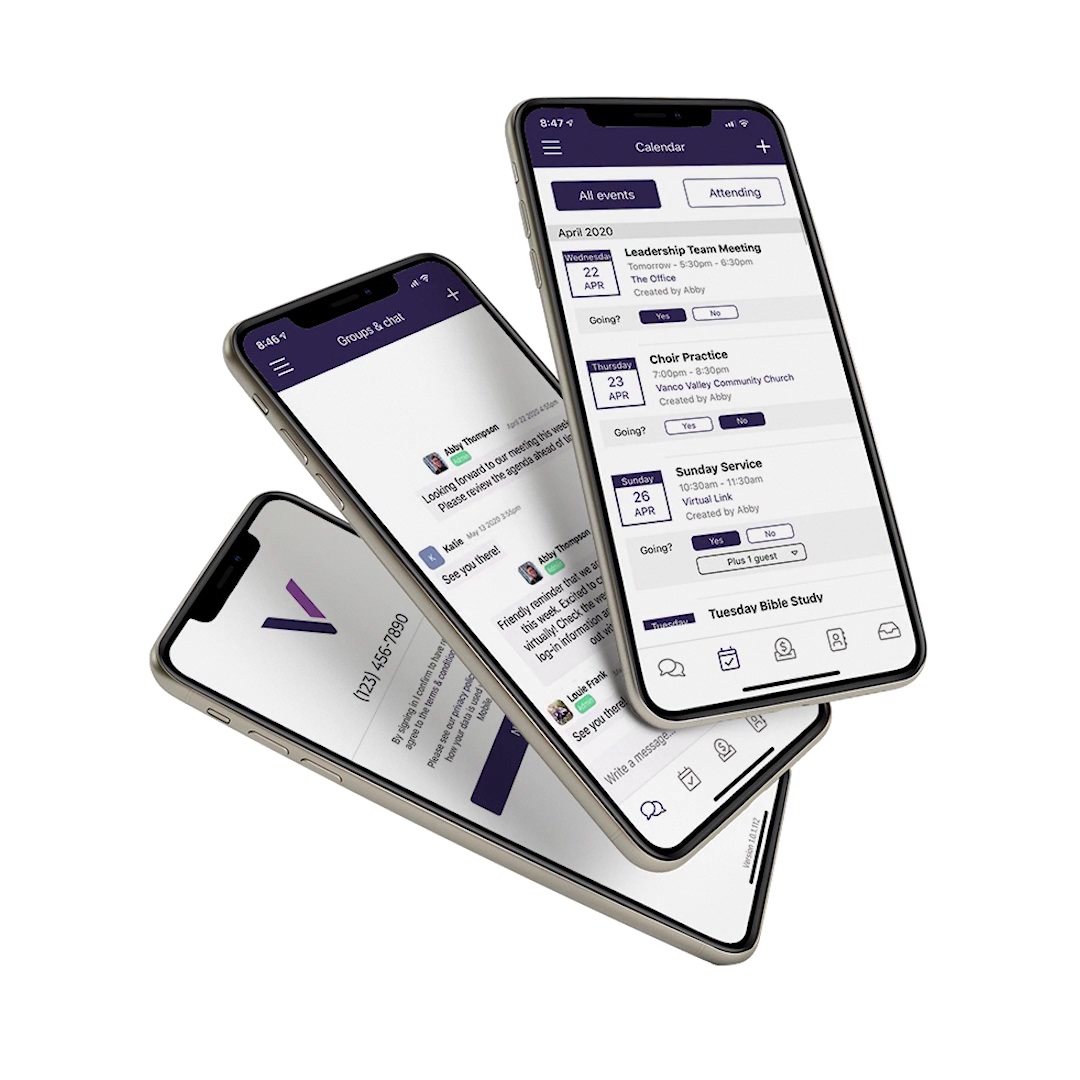

In the digital age, churches can leverage technology to foster growth and enhance connections with their congregations. One such tool is a mobile app, which offers numerous benefits ranging from improved communication to increased giving opportunities.

Benefits of a Church Mobile App

- Enhanced communication: A church mobile app enables effective, instant communication with your congregation. From sharing announcements to sending reminders about upcoming events, an app ensures your message reaches your audience promptly. Moreover, push notifications can act as gentle reminders about church activities and giving opportunities.

- Increased giving opportunities: Mobile apps make it easier for members to donate at their convenience. Whether it's a recurring tithe or a one-time donation toward a specific cause, a mobile app can automate and simplify the giving process, leading to increased contributions.

- On-demand access to resources: With a mobile app, sermons, spiritual resources and church leaders' notes are accessible anytime, anywhere. This on-demand access caters to members who missed a service and those who want to revisit a sermon for further reflection.

- Improved community engagement: Through features like prayer requests, event sign-ups and volunteer opportunities, a mobile app can foster a sense of community and encourage active participation.

Beyond Sunday Services: Engaging Members During the Week

A mobile app allows churches to extend their reach beyond Sunday services. By offering daily devotions, scripture readings and discussion forums, churches can engage members throughout the week.

Moreover, apps can be customized to fit each church’s unique needs. For instance, some churches might incorporate exclusive church songs for streaming, while others might have a section dedicated to missions and volunteering.

Implementation Tips and Getting Started

Implementing a mobile church app requires careful planning. Here are the steps to get started.

- Identify your needs: Understand what your church and congregation need from the app. This could be improved communication, increased giving or better community engagement.

- Choose the right developer: Look for a developer with experience in creating church apps. They should understand the unique needs of a religious institution.

- Promote your app: Once the app is live, encourage your congregation to download and use it. Highlight its benefits and features in your services and communications.

- Monitor and improve: Regularly assess the app's performance and seek feedback from users. Use this information to make necessary improvements.

35. Improve Your Virtual Services

In today's digital age, offering engaging and meaningful virtual services is crucial for attracting new members and fostering church growth. With the advent of online platforms, churches can reach beyond their physical walls to connect with individuals who may hesitate or be unable to attend in person.

Successful Virtual Services: Learning from Others

Churches worldwide are leveraging technology to offer a variety of virtual services. For instance, Life.Church has an extensive library of sermons, resources and apps available for free. Meanwhile, North Point Community Church and Saddleback Church are among the largest online churches, known for their high-quality streaming and interactive elements.

These successful virtual services have a few things in common. They use compelling visuals and graphics, offer a variety of content to cater to different age groups and interests, maintain consistent schedules and ensure their platforms are user-friendly.

Improving Your Church's Virtual Services: Action Tips

Drawing from these successful examples, here are some strategies to enhance your church's virtual services:

- Incorporate interactive elements: Engage your audience by incorporating interactive elements into your services, such as live chats, polls or Q&A sessions.

- Offer tailored programs: Cater to specific groups within your congregation by offering tailored programs, such as youth Bible studies or senior fellowship meetings.

- Optimize video quality: High-quality streaming is essential for a seamless viewing experience. Ensure your video and audio quality are top-notch.

- Frequent and consistent services: Regularly scheduled services give your congregation something to look forward to and help establish a routine.

- User-friendly platform: Ensure your platform is easy to navigate, with clear instructions on how to access various features and services.

Enhancing virtual services is a powerful strategy for church growth. By offering engaging and meaningful online experiences, you can attract new members, retain existing ones and deepen your connection with your congregation, no matter where they are.

If you’re unsure how to start planning how to grow your church, we built a free virtual ministry guide with insights on...

- Why virtual worship is essential for every church

- Building a strong foundation for your virtual ministry

- Creating an affordable virtual church home

- Budget-friendly and free tools for your online setup

- Steps to deliver a top-tier online church service

- Techniques for engaging members and guests beyond worship

Don't wait any longer! It's time to transform your church's reach. Download our eBook today and step into a new era of ministry excellence.